Home / Boards / CBSE / Important Questions / Class 10 / Social Science / Money and Credit

Table of Contents

Ans. (b)

Explanation:

In India, the Reserve Bank of India issues currency notes on behalf of the central government.

Ans. (d)

Explanation:

In an SHG most of the decisions regarding savings and loan activities are taken by its members.

Explanation:

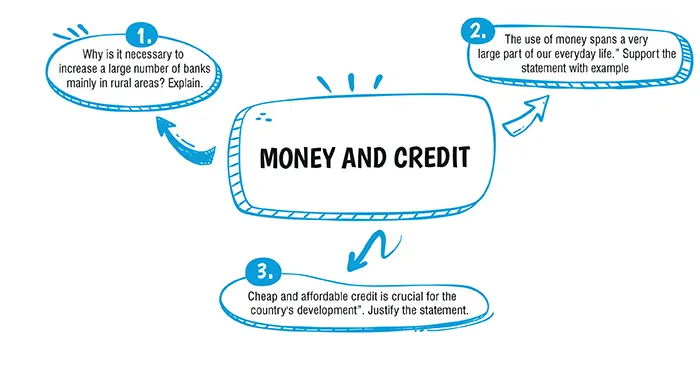

It is important to open more banks in the rural areas as the formal sector of credit is missing. The practice of borrowing from the informal sector that currently exists in rural areas, for example local moneylenders, has a number of disadvantages.

(i) The informal sector charges a higher rate of interest. Informal sector makes loans very expensive as there are no external organisations controlling the credit activities of lenders.

(ii) Informal sector involves a high degree of risk as there are no proper set of rules for repayment and there is a lot of exploitation of poor farmers.

(iii) Lenders may exploit the borrowers, they may engage in threats and intimidation to ensure repayment of loans. There is no written agreement between the lender and the borrower. There is no legal recourse in case of informal sources of credit.

Explanation:

The use of money spans a very large part of our everyday life and the following examples support it.

(i) Money has become an essential part of our lives. It is used to buy basic items like food, milk products, clothes, etc.

(ii) Money is used to pay for the services we enjoy. For example, the fee of a watchman, teacher, doctor, etc.

(iii) Money is also used for borrowing and lending like loans. Moreover, it is commonly used at places where there might not be any actual transfer of money taking place now but a promise to pay money later.

Explanation:

Importance of cheap and affordable credit for the country’s development:

(i) Cheap and affordable credit would lead to higher income.

(ii) Many people could borrow for a variety of needs

(iii) It encourages people to invest in agriculture, do business and set up small-scale industries etc.

(iv) It enables more investment which will lead to the acceleration of economic activities.

(v) Affordable credit would also end the cycle of the debt trap

| Chapter No. | Chapter Name |

|---|---|

| History | |

| Chapter 1 | The Rise of Nationalism in Europe |

| Chapter 2 | Nationalism in India |

| Chapter 3 | The Making of a Global World |

| Chapter 4 | The Age of Industrialization |

| Chapter 5 | Print Culture and the Modern World |

| Geography | |

| Chapter 6 | Resources and Development |

| Chapter 7 | Forest and Wildlife Resources |

| Chapter 8 | Water Resources |

| Chapter 9 | Agriculture |

| Chapter 10 | Minerals and Energy Resources |

| Chapter 11 | Manufacturing Industries |

| Political Science | |

| Chapter 12 | Power – sharing |

| Chapter 13 | Federalism |

| Chapter 14 | Gender, Religion and Caste |

| Chapter 15 | Political Parties |

| Chapter 16 | Outcomes of Democracy |

| Economics | |

| Chapter 17 | Development |

| Chapter 18 | Sectors of the Indian Economy |

| Chapter 19 | Money and Credit |

| Chapter 20 | Globalization and The Indian Economy |

Ans: Expanding formal sources of credit in India is crucial for two primary reasons. First, it helps reduce reliance on informal credit sources, which often impose high interest rates and offer limited benefits to borrowers. Second, by enhancing formal credit channels, a larger segment of the population can access loans, as many individuals have greater trust in government-sanctioned credit systems compared to private lending institutions.

| Chapter Wise Important Questions for CBSE Board Class 10 Economics |

|---|

| Development |

| Sectors of the Indian Economy |

| Money and Credit |

| Globalization and The Indian Economy |

CBSE Important Questions Class 10

ICSE Important Questions Class 10

CBSE Important Questions Class 10

ICSE Important Questions Class 10

CBSE

CBSE Important Questions

Important Questions Class 10

Class 10 Maths

Maths Science

Science Social Science

Social Science English

English Biology

Biology Physics

Physics Chemistry

Chemistry Computer Applications

Computer Applications History & Civics

History & Civics Geography

Geography Business Studies

Business Studies Economics

Economics Accountancy

Accountancy Political Science

Political Science General Test

General Test